on a journey to PMF: who am i selling to (hint: it's not a list of names or companies)?

I didn't actually know who I was selling to and that realization changed everything about how we're going to market at Journey.

Hey everyone,

Last week, I sat down with Steven Brady and we defined who Journey.io is actually for.

If you’d asked me a couple months ago who Journey’s ideal customer was, I would have given you a confident answer.

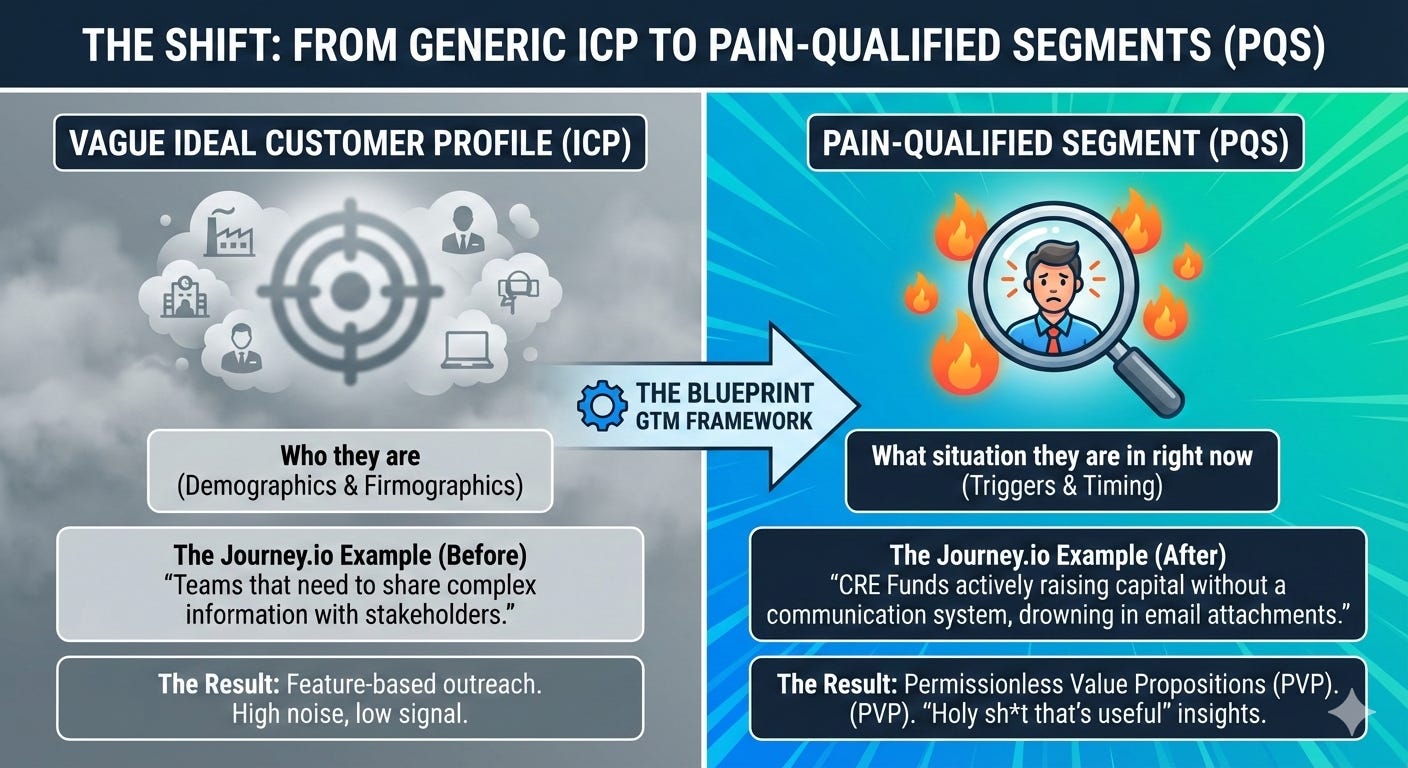

Something like: “Teams that need to share complex information with stakeholders and want to track engagement.”

Useless.

That description could be a CRE fund sharing deal memos with investors, a manufacturing company sending spec sheets to procurement teams, or a solo founder pitching with a Google Drive link.

All technically true. All completely different buying motions, pain points, and willingness to pay.

The issue wasn’t that we didn’t have customers.

We do.

The issue was that I couldn’t articulate why those customers bought, what specific pain drove them to us, or how to find more people in that exact same situation.

That’s the gap. And if you’re a founder reading this and you can’t answer those three questions for your best customers, you have the same gap.

Here’s what I’ve learned, and what we’re now building.

fun stuff (before we jump into things…)

With the boys sharing a room, I moved my office from the guest bedroom to the extra room that we have now. Still a bit of organizing to do, but it’s nice to have a bit of room (although I’ve subconsciously walked into the other room at least a half dozen times already this week).

enter PQS and PVP

Reading through Jordan Crawford’s Blueprint GTM methodology (here’s a Substack that talks about this), I got introduced to two concepts that I think every early-stage founder needs to internalize:

Pain-Qualified Segments (PQS) — These aren’t just ICPs. A PQS is a specific situation a specific type of company is in that creates a pain your product solves. The key word is “situation.” It’s not about demographics (industry, size, revenue). It’s about what’s happening to them right now that makes your product relevant.

Permissionless Value Propositions (PVP) — This is the outreach angle that proves you understand their pain before you ever ask for a meeting. A good PVP uses publicly available data to deliver an insight the prospect hasn’t connected themselves. It passes what I now call the “Holy Shit, that’s useful” test — from their perspective, not yours.

If you can’t define your PQS and build PVPs against them, it means you don’t deeply understand the value of your own product. Not in the way that matters for growth. You might understand it technically. You might have a nice features page. But you don’t understand it from the buyer’s chair — which is the only place that counts.

Here’s an example of a PQS and PVP:

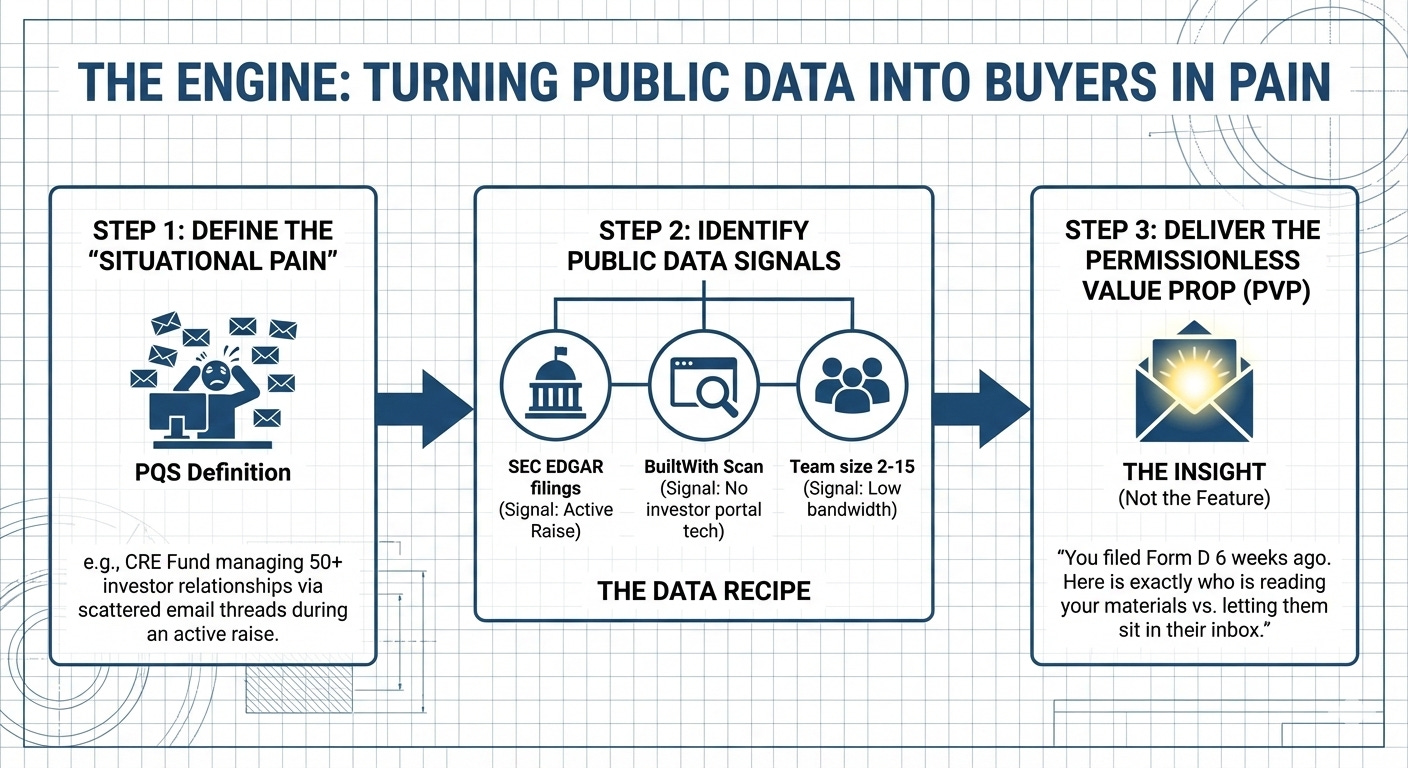

PQS #1: “New Fund Raising Capital Without a Communication System”

Ideal Customer Profile Experiencing Pain

Company: CRE fund or alternative investment firm, 2–15 employees, actively raising or deploying capital Persona: Founder / Managing Partner / VP of Investments Situation: Running a fund that communicates with 30–100+ investors per deal. Currently sending deal memos, webinar recordings, and quarterly updates via email attachments or shared drives. Every deal cycle means rebuilding the same email thread chaos from scratch.

Core Pain:

Sending 50–60 investors the same deal materials via individual emails or BCC blasts

No visibility into which investors actually opened/read the materials vs. ignored them

Investors reply-all or email back asking for documents already sent 3 weeks ago

6+ month fundraising cycles with no single source of truth — just scattered email threads

Can’t tier investor interest (who’s hot, who’s cold) based on engagement

Sharing sensitive financial documents via email attachments feels unprofessional and insecure

Pain Data Recipe

Data Point Source Timing Signal Fund currently raising capital (open fund or new vehicle) SEC EDGAR filings (Form D), AngelList, fund announcements Active raise or within last 90 days Using Dropbox/Box/Google Drive for investor documents Website tech stack (BuiltWith), job postings mentioning tools Current Investor base of 30+ LPs Fund size + minimum check size math, LinkedIn network Current NOT using Juniper Square or similar investor portal Website tech stack, job postings, G2 reviews Current (absence of signal) Small team (2–15 people) LinkedIn Company Page headcount Current

Why This Segment Matters to Journey Now

These funds are in active communication mode — they MUST get materials in front of investors consistently and professionally. Every missed open or buried attachment could mean a $25K–$150K+ check that doesn’t get written. Journey’s tracking turns investor communication from a black box into a tiered pipeline. We have a customer in this segment paying $500ish/month so it’s proof this segment pays premium and stays long-term.

Example PQS Message Hook

[Mirror] Noticed [Fund Name] is raising Fund II — congrats on the momentum. With 40+ investors to keep updated across a 6-month cycle, I’m guessing your inbox is becoming the de facto deal room right now.

[Insight] The investment firms we work with that manage 50+ investor relationships found that the biggest leak in their fundraise wasn’t deal quality — it was communication visibility. They had no way to know which LPs actually read the deal memo vs. which ones let it sit in their inbox. The ones who closed faster started using a single evolving link per deal instead of email threads — it let them tier investor interest by engagement and follow up with the right people at the right time.

[Ask] Curious how you’re currently tracking which investors are actively engaging with your materials vs. going quiet?

PVP 1.1: “Your Form D Says You’re Raising — Here’s Who’s Reading Your Materials”

Rating: Gold Standard

Target Persona: Managing Partner / Founder of CRE fund Core Insight: SEC EDGAR Form D filings are public. When a fund files a Form D (Regulation D exemption), the raise amount, date, and executive names are on record. Cross-reference this with whether the fund has any investor-facing content platform (BuiltWith scan) and you can identify funds actively raising capital with no engagement visibility system. Data Basis: SEC EDGAR Form D filings + BuiltWith tech stack scan + LinkedIn headcount Value Proposition: “You filed your Form D 6 weeks ago for a $15M raise. Based on your web stack, you’re managing investor communications through email. Here’s what that looks like from the investor’s side — and what the funds closing faster are doing differently.” Low-Effort CTA: “Want me to build a sample investor Journey using your fund’s public materials so you can see the difference? Takes 10 minutes to set up, zero from you.”

what this can look like in practice

We mapped Journey’s market into three ICPs: Commercial Real Estate / Finance, Manufacturing / Industrial Products, and Founder-Led B2B Services.

Within each, we defined Pain-Qualified Segments — not just “who they are” but “what’s happening to them right now.”

For CRE funds, one of our PQS targets is: “New fund raising capital without a communication system.” That’s a fund with 30–100+ investors, actively raising, currently managing deal memos and quarterly updates via email attachments and shared drives. Every deal cycle, they rebuild the same email chaos from scratch. They can’t tell which investors actually read the deal memo vs. which ones let it sit in their inbox.

The timing signal? SEC EDGAR Form D filings. When a fund files, the raise amount, date, and exec names are public record. Cross-reference that with a BuiltWith scan showing no investor portal, and you’ve identified a fund in active pain with no system.

For manufacturing companies, one of our segments is: “Complex product, can’t demo on Zoom.” These are companies with 7+ product lines, 40+ spec sheets, beautiful renderings on their website — but the moment a sales rep needs to share materials with a prospect, it all becomes email attachments. They’ve got HubSpot but no content platform between marketing and sales.

The data recipe here is scraping product pages, counting downloadable assets, checking the tech stack for sales enablement tools (Highspot, Seismic, Showpad), and confirming the gap.

For founder-led services, we’re looking at founders sharing portfolio work via Google Drive links on LinkedIn. The PVP here is almost absurdly direct: take their public work, rebuild it as a Journey with proper visual presentation, and send them the before/after. Their prospect currently sees “ClientX_Reel_Final_v2.mp4.” We show them what it could look like instead.

the humbling part

The thing that really hit me during this process was realizing how much of our positioning was so generic.

That’s the difference between “Journey helps you track engagement on shared content” and “Your last webinar had 75 registrants. The recording on YouTube has 23 views. That means roughly 52 investors who were interested enough to register never watched. And you have no idea which 52.”

The first is a feature statement. The second is a PVP.

One gets ignored. The other gets a reply.

Our highest-paying customer, who’s in the CRE segment, didn’t come to us because of a cold email about features. They started using Journey for webinars and community content, then expanded to all investor communications. They now power every LP touchpoint through Journey. That journey (no pun intended) from entry point to full adoption is the exact path we need to engineer for new customers and the PQS/PVP framework gives us the map.

will it work is my question

I don’t know, but this is all a forcing function because if it doesn’t work it just means that Journey is just noise and another generic SaaS tool without a specific corner of the market.

If you’re a founder still operating with a vague ICP and sending generic outreach, I’d encourage you to do the exercise we just did. Ask yourself: for your three best customers, what specific situation were they in when they bought? What was happening in their business that made your product urgent? And can you find more people in that exact same situation using publicly available data?

If you can’t answer those questions, you don’t have a targeting problem. You have an understanding problem, a positioning problem. And no amount of volume is going to fix it.

That’s what I’m working towards…

Cheers,

Danny

You've really internalized this well and taught it back excellent through this piece. Looking forward to getting more data (and ideally validation) from the market with this motion.

this is excellent - your memos are getting sharper and sharper as you learn and grow this thing!